“When you want to brag about a stock, you should sell it!”

– John Neff-former Portfolio Manager at Vanguard Windsor

Dear fellow investors,

Warren Buffett released his 2021 Berkshire Hathaway Annual Letter on Saturday, February 26, 2022. He seemed to want to talk about almost anything besides the stock market. Corporate income taxes, whole company purchases in Lubbock, Texas (TTI, BNSF), Berkshire Hathaway (BRK) stock buybacks and excitement of throwing the in-person annual meeting in April of 2022 topped the list.

The rest of the letter was dominated by emphasizing the four main “giants” of the business. The insurance businesses, Apple (AAPL) shares, Burlington Northern Railroad and Berkshire Energy make up a huge part of total earnings. However, Apple is the only publicly-traded company among the four giants.

It reminded us of the 1996 Annual Letter which came out in February of 1997. Here is what Buffett wrote:

Companies such as Coca-Cola and Gillette might well be labeled “The Inevitables.” Forecasters may differ a bit in their predictions of exactly how much soft drink or shaving-equipment business these companies will be doing in ten or twenty years. Nor is our talk of inevitability meant to play down the vital work that these companies must continue to carry out, in such areas as manufacturing, distribution, packaging and product innovation. In the end, however, no sensible observer – not even these companies’ most vigorous competitors, assuming they are assessing the matter honestly – questions that Coke and Gillette will dominate their fields worldwide for an investment lifetime. Indeed, their dominance will probably strengthen.

Here is what he wrote about Apple in the 2021 Annual Letter:

Apple – our runner-up Giant as measured by its year-end market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier. That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job. It’s important to understand that only dividends from Apple are counted in the GAAP earnings Berkshire reports – and last year, Apple paid us $785 million of those. Yet our “share” of Apple’s earnings amounted to a staggering $5.6 billion. Much of what the company retained was used to repurchase Apple shares, an act we applaud. Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well.

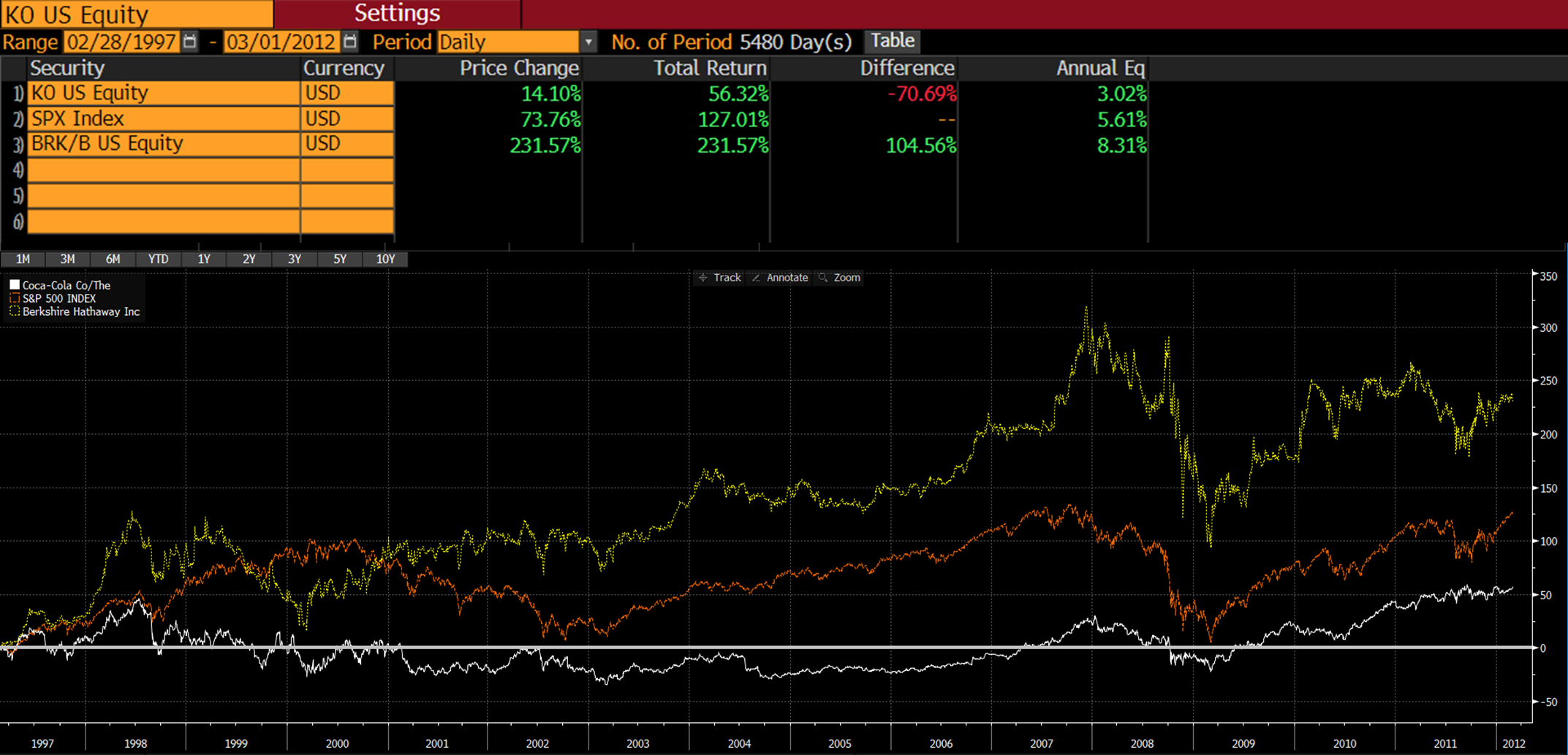

Look at the chart of Coca-Cola (KO) stock from March 1, 1997, to March 1, 2012:

While Buffett was beating his chest, he was punishing his future capital base. KO effectively knocked out some of Berkshire’s success and underperformed the S&P 500 Index substantially. It even more dramatically underperformed Berkshire Hathaway shares. Lastly, he could have doubled the return on KO from buying the five-year Treasury bond. As you can see below, the price-to-earnings (P/E) ratio of KO contracted in those 15 years:

- P/E on 03/01/1997: 47.29x

- P/E on 03/01/2012: 18.04x

Therefore, Buffett would have been better off in 15 years by selling the “inevitable” Coca-Cola shares and buying back shares of his own company with the money. Notice how KO did from his purchase in 1988 to the 1996 Annual Letter:

Let’s look at how Apple’s shares have done the last seven years from February of 2015 to February of 2022:

AAPL P/E Ratios:

- P/E on 02/02/2015: 16.04x

- P/E on 02/01/2022: 28.95x

This brings us to our main point. Buffett is highlighting his best performing, publicly-traded common stock (like he did in 1997). Berkshire Hathaway has been sitting on a monstrous pile of cash since 2020, along with most other investors who were scared. Buffett says, “be fearful when others are greedy and greedy when others are fearful.” We would add be fearful of mature growth companies, which have had great runs in the stock market! This would be especially true when interest rates go down and T.I.N.A. (There Is No Alternative to stocks) dominates the landscape. Will Buffett make the same mistake going forward with Apple shares that he made with Coca-Cola shares? As always, fear stock market failure!

Warm regards,

William Smead

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2022 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.