Dear fellow investors,

Recently, we had dinner with some of our grandchildren and they ordered macaroni and cheese. The recent advertisement goes, “Kraft Mac and Cheese, the best thing ever!” For most investors in the stock market, the S&P 500 Index has been the best thing ever over the last 17 years and terrific since the bottom of the stock market in 1982. History would argue that investing in popular securities and heavily concentrated versions of the S&P 500 over history has been the worst thing ever for investors!

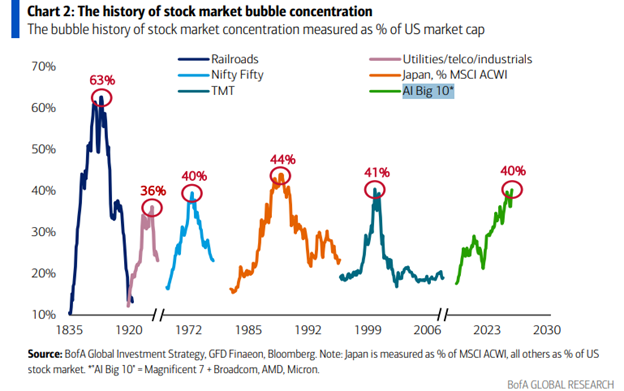

Here are some of the most concentrated markets in the past two centuries:

Some of the worst market declines in history have occurred in our 45 years in the stock market (1987, 2000-2003, 2007-2009 and 2020). However, the 1987 and 2020 declines lasted just 78 and 60 days and fully qualify as cases of fast death. The other two were 50% declines in the S&P and, in 2000-2003, included NASDAQ annihilation. Nobody survived the 85% decline in Amazon’s stock from December 27, 1999, to the bottom in 2003. Therefore, since 1981, when long-term Treasury interest rates peaked at 15%, the S&P 500 Index has had a massive tailwind from the reduction in the risk-free interest rates. Cheap stocks in 1982 and constantly declining interest rates were the BEST THING EVER!

Where are we now? Interest rates are rising, and probably the only thing that would bring those interest rates down would be a massive sell-off in the S&P 500 Index. Why do we say that? We say it because that is where the money is, and it won’t move to safety until the Index gets slaughtered. The Index will get slaughtered because it is massively over-weighted in technology and tech-related stocks to the tune of 50%.

Michael Hartnett, Managing Director and Chief Investment Strategist at BofA Global Research, says this is even starting to dwarf what happened in 2000: “What makes the current advance particularly striking is not the level of the major indices but the extraordinary narrowness beneath the surface. The S&P 500 may be printing fresh highs, yet only 21 companies, roughly 4% of the index, are making new highs alongside it, he stated.” Hartnett notes that the number was almost identical at the peak of the dot-com bubble in March 2000.

We know that Charlie Munger said, “Envy is a really stupid sin because it’s the only one you could never possibly have any fun at.” When Bezos asked Buffett in a recent conversation why more people don’t simply copy his straightforward investment thesis, Buffett bluntly replied, “Because no one wants to get rich slowly.” We are going to trust patience and avoid envy until this phase breaks.

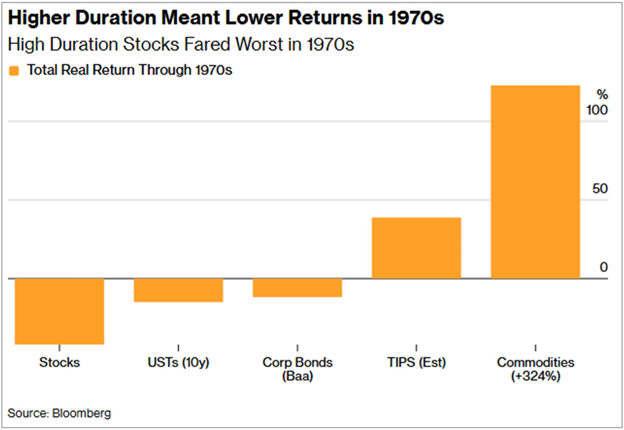

What can do well in this monstrously expensive S&P 500 Index in a decade of heartache? Look no further than the 1970s. The Yom Kippur War came right after the top in the Nifty-Fifty concentrated bubble stock market:

We are expecting inflation in energy prices and a decline in interest rates when the poop hits the AI mania fan. For these reasons, we are overweight in oil stocks and home builders. These industries prospered in the 1970s, once the stock market mania broke in late 1972!

As always, play the long game!

William Smead

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, Chairman & CIO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2026 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com