Dear fellow investors,

On April 12, 2019, Chevron (CVX) and its CEO, Mike Wirth, offered $33 billion dollars to buy the common shares of Anadarko Petroleum. They stood to assume $17 billion in existing debt at a time that WTI crude oil was trading for $65 per barrel. Here is what Chevron’s CEO Mike Wirth said at the time:

“What was great just gets better,” Mr. Wirth said in an interview Friday. “We think this is a terrific fit.”

As we write this on January 21 of 2022, oil is trading around $84 per barrel. Occidental Petroleum (OXY), the owner of Anadarko Petroleum, is trading around $34 per share for a market cap around $32 billion and has about $27 billion of debt outstanding. OXY was trading in 2019 around $49 billion in market cap with about $11 billion in debt outstanding. The debt of OXY today is about the same as Anadarko and OXY had combined back then. However, the buyer of OXY now gets the 2019 market value of Chevron’s offer for Anadarko of $33 billion and prices OXY’s market value at $9 billion.

Here are how the numbers back in April of 2019 broke down:

- OXY Enterprise Value: $49 billion market value and $11 billion in debt = $60 billion enterprise value

- Anadarko’s Enterprise Value: $33 billion market value and $17 billion in debt = $50 billion to Chevron

- Total Enterprise Value of OXY/Anadarko: $110 per share at $65 per barrel of oil

- OXY Enterprise Value January 21, 2022: $32 billion market value and $27 billion in debt plus $10 billion in Berkshire Hathaway preferred shares = $69 billion at $84 per barrel of oil

You might ask: what is the difference between the $65 oil of 2019 and the $84 oil of today other than the price? First, the body politic is seeking to restrict the uses and future production capability of the most abundant and economic energy source which exists. Second, the marketplace thinks that a quicker transition away from fossil fuels can happen. We again remind you of what Warren Buffett said at his May 2021 annual meeting as the owner of the largest energy utility in the country:

“The people who think we will make a quick transition away from fossil fuels and those who think we will never transition are both crazy!”

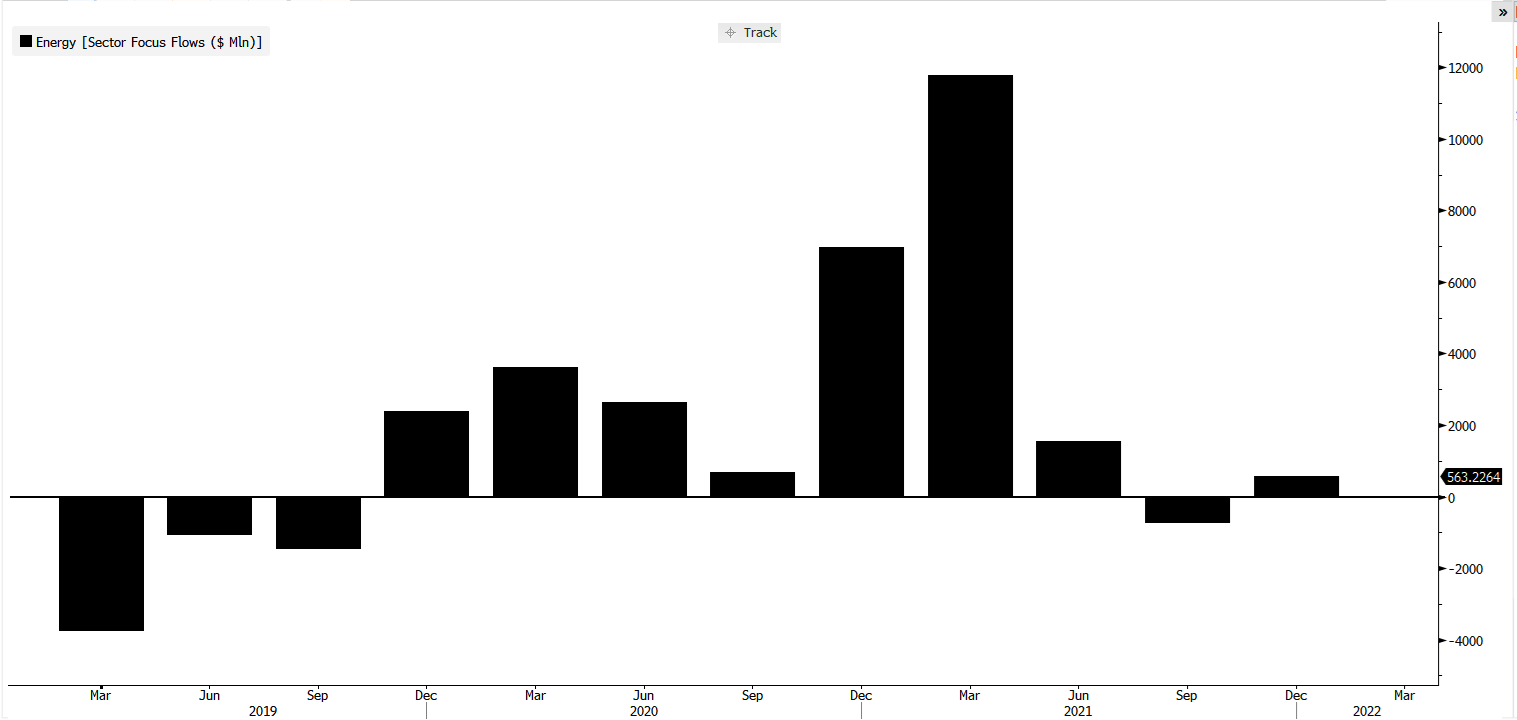

Third, a major investment boondoggle called ESG, designed to lace the pocketbooks of investment product providers, is dominating investment fund flows. See the chart below:

We believe that ESG is formed primarily to entice investors into accepting sub-optimal long-term returns via dramatically higher fees through investment selection restrictions. It seeks to be morally virtuous. The pressure that this has put on participants in the capital markets is intense, because hardly anyone is willing to make investments in the fossil fuels. We will need that fuel for the next twenty years to get us across the valley to the potentially cleaner forms of energy. This would be when the environmentally cleaner energy sources can be aggregated at a level to dominate overall consumption.

The last difference is interest rates. They were significantly higher in 2019, when Mike Wirth and Chevron were going to borrow the money to buy Anadarko. In theory, that should cause the business to be valued higher today. The 10-year Treasury interest rate was around 2.5% at the time, and today’s interest rate is around 1.77%.

In the meantime, executives at the major oil companies have two choices. 1) They can kowtow to the ESG capital flows and spend all their future investment dollars on becoming carbon neutral, or 2) they can potentially make a pile of money meeting the economic need for the next twenty years and then figure out what to do with the money when they are done. OXY has some of the most respected carbon capture efforts in place among major oil producers.

This brings us to Chevron CEO, Mike Wirth. So far, he has neither joined with the European oil producers, who have drunk the ESG Kool Aid. Nor has he led the company to take full advantage of the stock market circumstances/low interest rates and followed up on what he believed was a “perfect fit” nearly three years ago. He needs to figure out what Chevron is going to be. Will he be like the European major oil producers or will he seek to be an oilocrat like Harold Hamm?

This is a seminal moment in the history of Chevron and of the entire energy complex. Since the other major players like Exxon, Total, Shell and BP are locked in place by the ESG feather dust, the door is wide open for Chevron. When the Pope and Elon Musk agree that we need more people, that feather dust looks out of line.

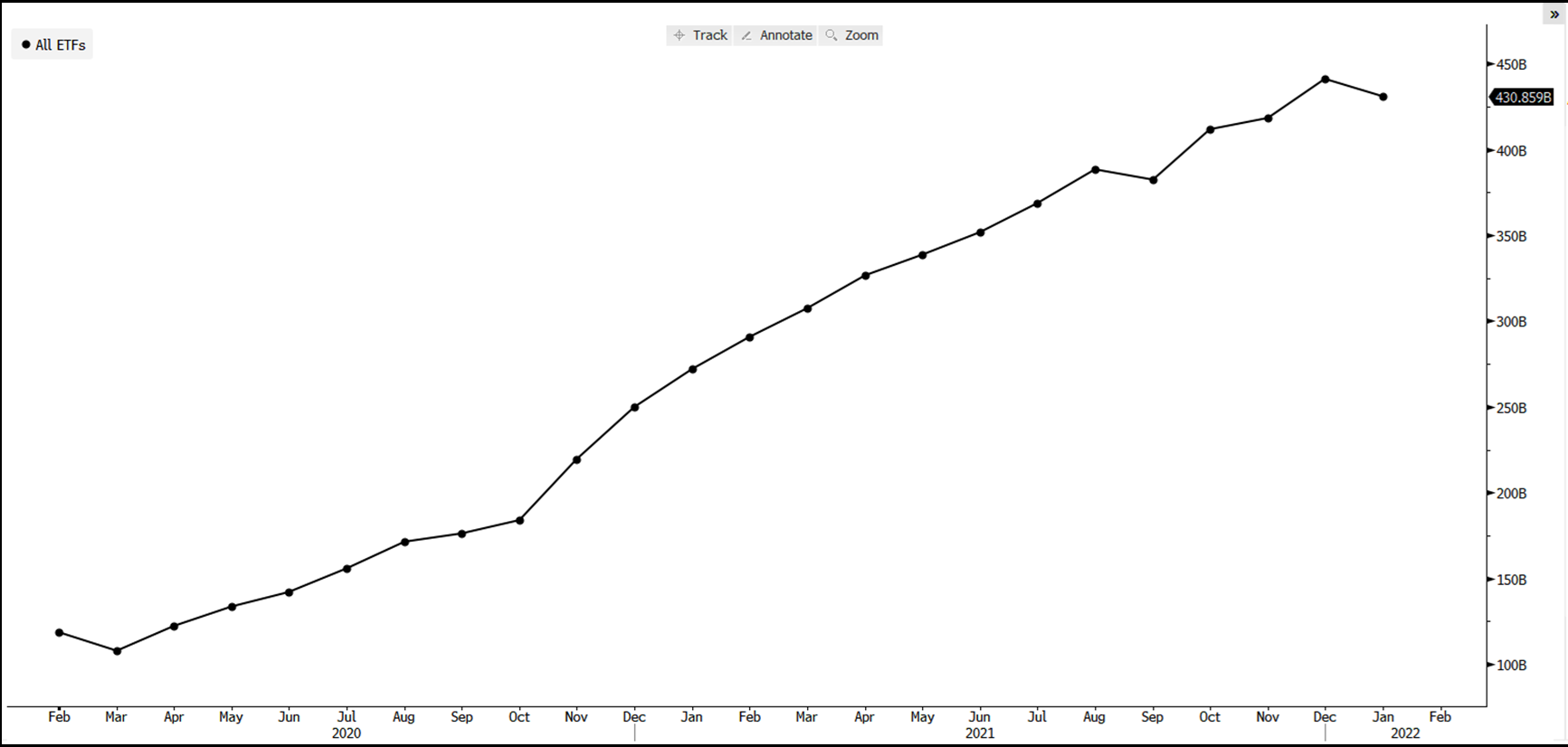

Chevron can do what Richard Bernstein calls “investing like the mafia.” The mafia invested where nobody else wanted to invest, because to do so was breaking the law. Since they were the only investor, the returns Mafia people like the “Godfather” demanded were very high. Below is a chart of flows into energy ETFs:

An ocean of $430 billion has flowed into ESG ETFs, while energy has attracted a few billion dollars. In our opinion, acquiring OXY/Anadarko at this juncture could be Chevron’s best hope to be a success in business over the next twenty years.

We believe the actual worth of Occidental Petroleum is far higher than the market participants are giving it today. Fear stock market failure!

Warm regards,

William Smead

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2022 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.