Printable Version

Printable VersionThe current circumstance in the U.S. stock market reminds us of the mid-1960s. We thought it would be helpful to review what was going on back then and what took place in the following 16 years. It makes us believe that you want to own wonderful businesses and de-emphasize trust in the stock market’s ability to meet the financial goals of long-duration investors.

The recent movie, Hidden Figures, told the story of the important part played by a group of African-American women in the NASA space program. The space race with the Soviet Union started in the late 1950’s and had full momentum by the mid-1960s. The work associated with putting a man on the moon caused a massive scientific effort which laid the groundwork for numerous exciting new technologies.

Coincident with the major push in science and technology came a roaring multi-decade stock market move. By 1966, companies were so well rewarded for being associated with technology that they were adding the letters o-n-i-c-s to their name. David Dreman explained this in his book, Psychology and the Stock Market:

Dreman describes a speculative mania in “-onics” stocks in the early 1960s during which short-term traders called gunslingers made and lost fortunes: “The more esoteric the concept, the better the public liked it. Any company ending in ‘-onics’ was almost guaranteed an enthusiastic reception.”

What the space race had done for tech in the 1960s, the internet might be doing for it today. Tech is once again so popular among investors that technology-based companies don’t even need to become public companies anymore to get rewarded multi-billion-dollar market capitalizations. The confidence in tech and the confidence in the U.S. stock market have gone hand in hand as they did in 1966. In a stock market dominated by technology and indexing in 2017, why would we want to consider common stock investing in 1966?

Commonalities between 1966 and 2017 include the following:

- P/E ratios in the high teens

- Interest rates moving higher (Federal Reserve tightening)

- Confidence in technology

- Early stages of household formation and home building

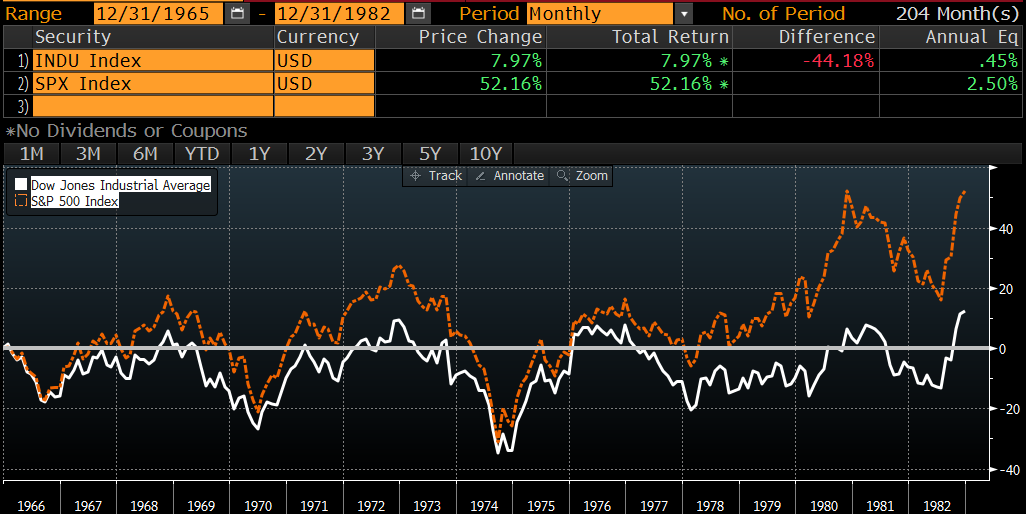

Source: Bloomberg. Data for the time period 12/31/1965 – 12/31/1982.

The tech dominated stock market of 1966 was the beginning of a relatively dismal period for index investors. The S&P 500 Index gained an average annual return of 2.50% from the beginning of 1966 to the end of 1982. The Dow Jones Industrial Average fared even worse, with a miniscule gain of 7.97%, which annualizes at 0.45%. Investors in 1966 earned an average of 4.00% in dividends through the end of 1982 for a total return of 6.80% (pre-expenses). The problem for index investors in 2017 is that today’s 2.00% initial dividend is significantly below the dividend offered in 1966.

If 2017 proves to be the beginning of a difficult era for index investors, as 1966 proved to be, how might disciplined long-duration large-cap value investing do going forward?

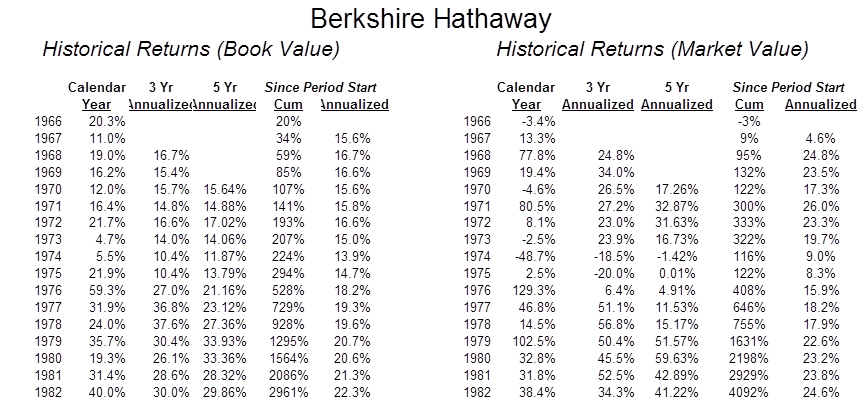

The answer could come by looking at the average return of the Large Cap Value equity funds found in Morningstar’s database from January 1, 1966 to December 31, 1982. An investment of $10,000 on January 1, 1966 grew to $42,814 as opposed to a gain to $29,256 in the S&P 500 Index. This is confirmed by looking at the movement of Berkshire Hathaway’s shares during that time period in the accompanying table:

Source: Berkshire Hathaway Annual Report. Data for the time period 1/1/1966 – 12/31/1982.

The 17-year gain in Berkshire Hathaway shares was rudely interrupted by a greater than 50% decline in 1973 through 1974. However, it is obvious that the overall challenging index environment included a number of fire sale declines which opened the door for what most people consider to be the most successful value stock investor in U.S. investment history to thrive. We are not arguing that we have ability which rivals Buffett or that we are guaranteed to match the average of our peers in a better value environment. Instead, we are proposing that a more difficult index environment could open up opportunities to find meritorious companies on sale which meet our eight criteria for common stock selection.

The severe decline of 2007-2009 were profitable for us for the calendar years 2009 through the first quarter of 2017, even though most investors were acting as if the financial meltdown would keep us depressed forever. Think of all the negative nabobs who scared investors away from stocks the last eight years. We chuckle when we see them get trotted out on TV every time a decline happens in the S&P 500 Index. For us, an occasional bear market usually spells portfolio upgrade and long-duration opportunity, because our competitors and most individual investors see their trust in common stocks fall as prices fall.

This view of large cap value investing shows that money can be made and economic benefit can accrue in contrarian value strategies during an era of relatively poor index results. What evidence is there for similar forward improvement over the index?

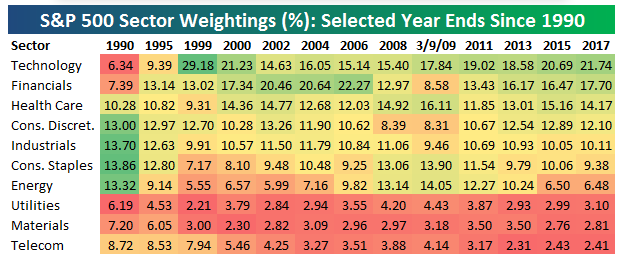

First, expensive stocks are dominating the S&P 500 Index and tech is the largest sector in the index. We would argue that the internet has been as important to investor views today as the space race was in the 1960s.

Source: Berkshire Hathaway Annual Report. Data for the time period 1/1/1966 – 12/31/1982.

Tech sector weighting

Source: https://seekingalpha.com/article/4054803-s-and-p-500-sector-weights-lot-changed-8-years. Data for the time period 1/1/1990 – 1/1/2017.

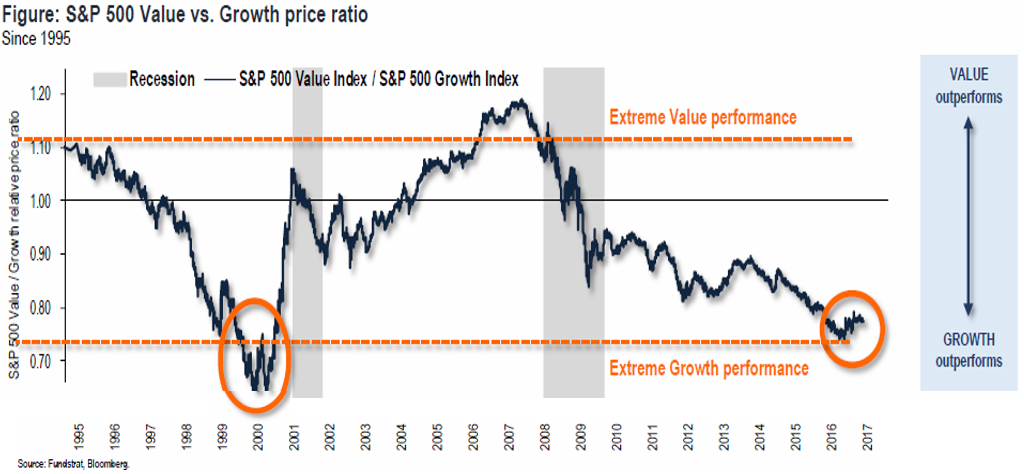

Second, growth strategies have stomped value strategies for nine years; one of the longest streaks ever.

Source: Fundstrat Fall 2016 “State of the Market”, page 72. Data for the time period 1/1/1995 – 1/1/2017.

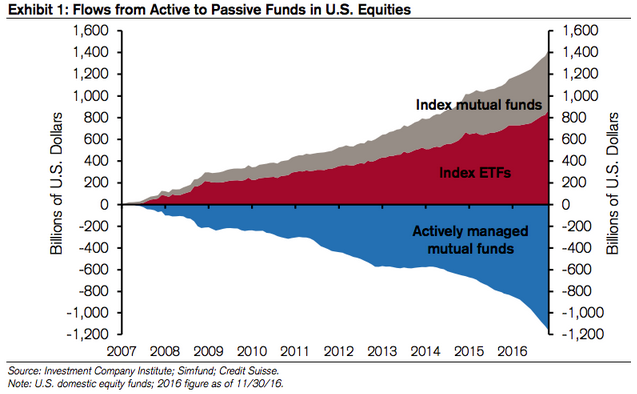

Third, money flows have exploded towards indexing.

Source: http://www.marketwatch.com/story/how-can-active-fund-management-be-dead-if-indexing-represents-only-5-of-all-assets-2017-01-13. Data for the time period 1/1/1990 – 12/31/2016.

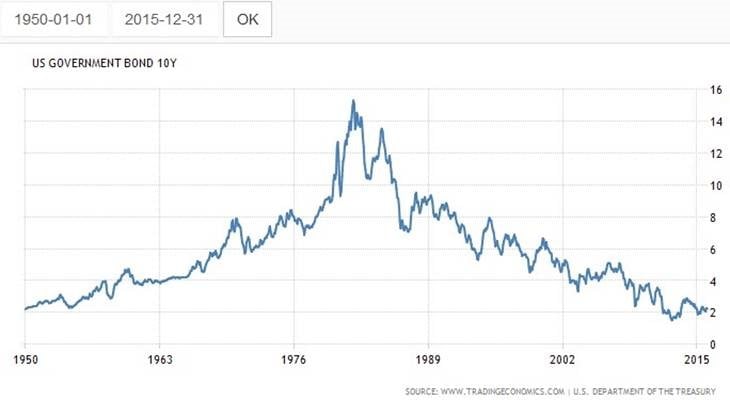

Fourth, interest rates appear to have bottomed on a secular basis. History argues that P/E ratios come down as interest rates rise and that was the case in the 1966 to 1982 experience. The S&P 500 Index had a high-teens P/E ratio in 1966 and bottomed with a single-digit multiple in 1982.

Source: U.S. Department of Treasury. Data for the time period 1/1/1950 – 12/31/2015.

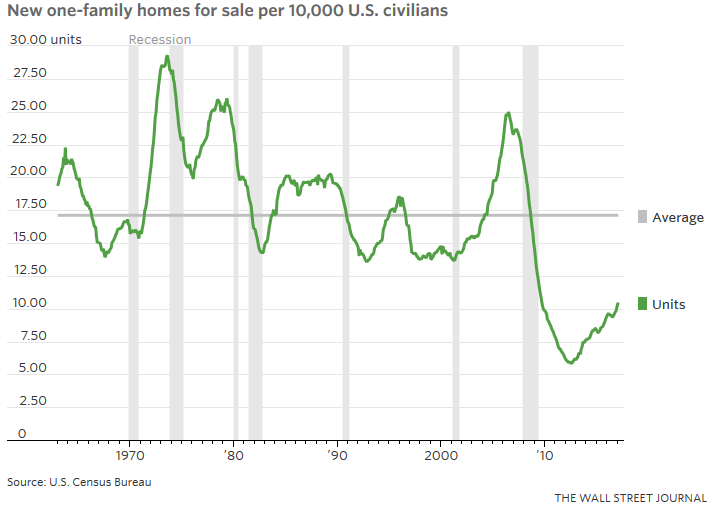

Lastly, the biggest demand driven boom in home building occurred in 1975-1980. In fact, one in ten single-family residences lived in in the U.S. today was built between 1975 and 1980.

Source: https://www.wsj.com/articles/what-will-the-housing-market-do-next-1491211806. Data for the time period 1/1/1960-12/31/2016.

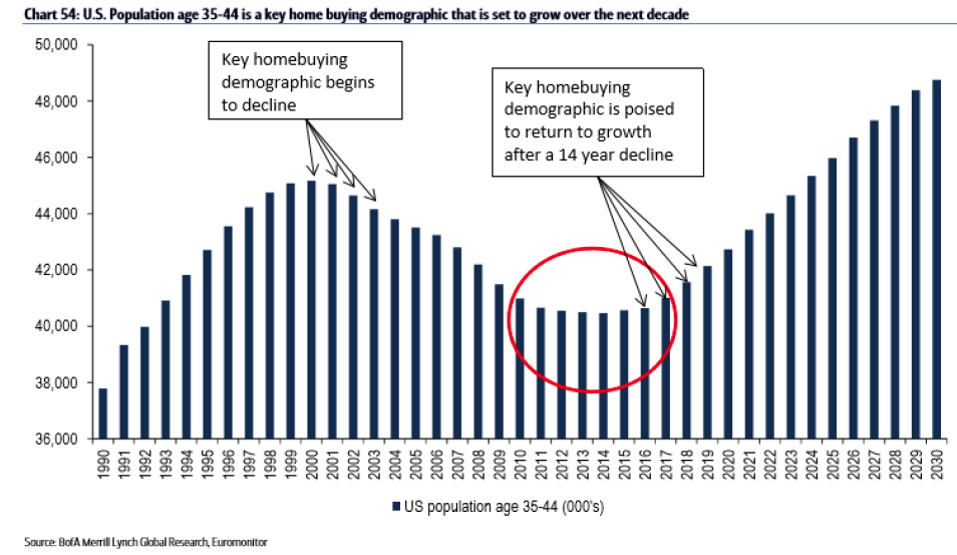

A home building boom is on its way as the number of American households with two children explodes on the back of aging millennials.

Source: BofA Merrill Lynch “Tracking the U.S. Consumer, September 16, 2016.

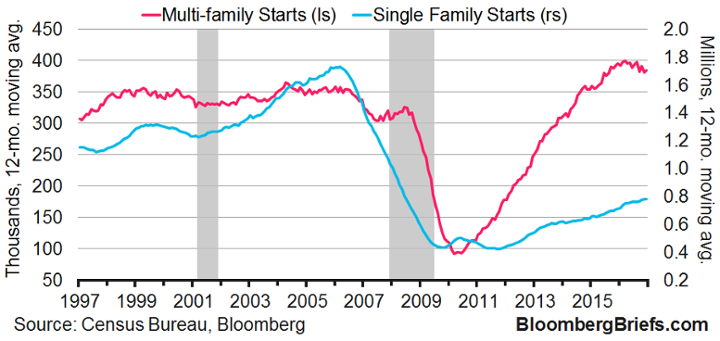

As single 27-year-olds move into their 30s, renting should go by the wayside or renting a house will become the default choice for renters.

Source: Bloomberg. Data for the time period 1/1/1997-12/31/2016.

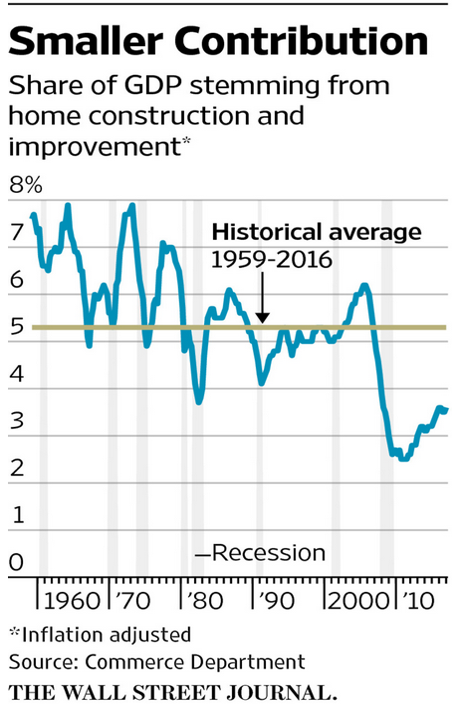

The hugely positive effect this would have on the U.S. economy was brought up recently by The Wall Street Journal:

Source: The Wall Street Journal. GDP: Gross Domestic Product. Data for the time period 1/1/1960-12/31/2016.

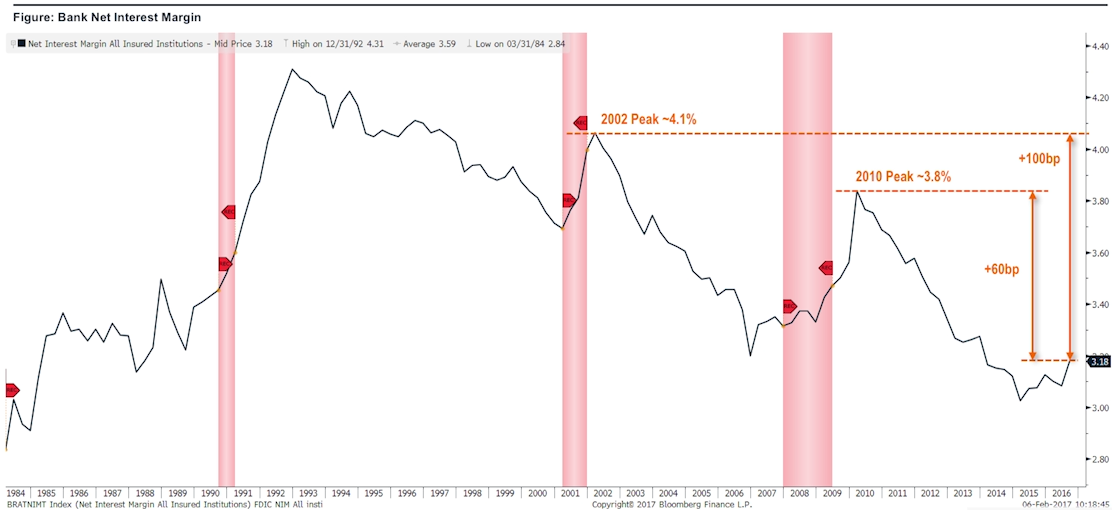

The impact of having the largest adult population group borrow the money to buy houses could cause interest rate spreads to improve dramatically for banks and insurance companies.

Source: Fundstrat / Bloomberg, Data for the time period 1/1/1994-12/31/2016. Shaded areas represent historical recession time periods. The end of the red arrows mark the start and finish of the recessionary periods.

We’ve given you quite a bit to think about. First, there have been situations like this in U.S. economic history and a similar one was 1966. Second, those who rely on the S&P 500 Index for returns which make their financial plans work must set lower assumptions than normal. Third, it is an above-average probability that contrarian, value stock picking strategies could have the wind at their back. Lastly, economic strength from household formation, child bearing and home buying could create prosperity for stock portfolios concentrated in companies tied to that prosperity.

We are over-weighted in Financials and Consumer Discretionary companies which could be major recipients of the forward economic momentum and own these meritorious companies at reasonable prices. We look forward to the coming years even if the tailwind the index has provided becomes an occasional headwind. Thank you for your trust and confidence as we work our way through 2017 and into the future.

A basis point is one hundredth of one percent.

First Call: A company that gathers research notes and earnings estimates from brokerage analysts. The estimate is compared to the actual reported earnings, and then the difference between the two is the earnings surprise.

The price-earnings ratio (P/E Ratio) measures a company’s current share price relative to its per-share earnings.

The information contained herein represents the opinion of Smead Capital Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Washington. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

For additional information about SCM, including fees and services, send for our disclosure statement as set forth on Form ADV from SCM using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

This Newsletter and others are available at smeadcap.com