Dear fellow investors,

We are closing in on what we think may be the question of the decade. If a majority of stock market capitalization in the US is passive or indexed, does this cause problems for stock markets? Bloomberg columnist John Authers addressed this conundrum by saying, “Logic dictates that not all assets could be run passively. If that were to happen, the market would stop functioning and cease to have any use in pricing and allocating capital.” We disagree with the ceasing to function. Markets were made by God to clear, but one question remains: at what price?

Last week, we were doing a podcast with CNBC’s NYSE correspondent Bob Pisani, on his newest book Shut Up and Keep Talking (great book by the way). and we asked him about this. We invited the discussion of how a majority of large-cap stocks being indexed causes structural issues in markets. Bob pushed back on this and pointed out that structural changes have taken place a myriad of years during his career. The old guard back then would have said it would never work each time, but markets continued along.

In other words, markets continue to function despite structural changes. Authers is missing the point according to Pisani, as well as William Sharpe. Markets function, but the investor’s question is related to price.

Should everyone index everything? The answer is resoundingly no. In fact, if everyone indexed, capital markets would cease to provide the relatively efficient security prices that make indexing an attractive strategy for some investors. All the research undertaken by active managers keeps prices closer to values, enabling indexed investors to catch a free ride without paying the costs. Thus there is a fragile equilibrium in which some investors choose to index some or all of their money, while the rest continue to search for mispriced securities.

Should you index at least some of your portfolio? This is up to you. I only suggest that you consider the option. In the long run this boring approach can give you more time for more interesting activities such as music, art, literature, sports, and so on. And it very well may leave you with more money as well.

Sharpe wasn’t worried about markets ceasing to function. He was worried that “markets would cease to provide the relatively efficient security prices” and active managers keeping “prices closer to values.” As Ben Graham said, “Price is what you pay. Value is what you get.” He never mentioned markets functioning as a requirement. This is assumed as a constant variable. Markets are always clear.

We agree with the passive community that markets will function as needed, no matter how high passive becomes in the ownership table. However, none of this decides what price you pay. We find too many people believing they can’t do damage to themselves with passive investments over longer periods of time. We believe the data argues Pisani’s case for markets clearing, but against good returns if price isn’t a factor. If you are in the Jeremy Siegel Stocks for the Long Run camp, beware of the next chart.

We continue to share this with the investors of Smead Capital Management because we should practice ignorance avoidance. When you look at the American household ownership of stocks as a percentage of their net worth, we are no longer at the worst moment in the last 70 years (pyrrhic victory). However, we are still at one of the likely poorest 10-year forward returns standpoints. If inflation runs at 5% in this decade, the odds of success in real terms still remain frustratingly low or unlikely. Even in indexes, investors’ money pours in at tops and flees at bottoms. Humans can’t change their stripes.

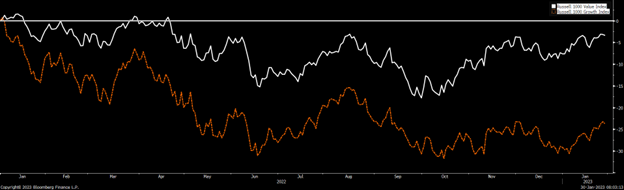

What would increase the investors’ odds of success in stocks? Be stingy on the price you pay for stocks. Fear stock market failure. Don’t go to Jonestown with the cult of stocks. How big do we believe the price aspect of this discussion is? Let’s use obtusely blunt objects to figure this out. Below is a chart of the Russell 1000 Growth and the Russell 1000 Value since equity ownership peaked at the end of 2021.

We call these ‘blunt’ because cheap stocks have severely outperformed their expensive brethren. Cheaper prices yielded a benefit of 20% since the end of the recent mania.

We want all the investors of Smead Capital Management to know that capitalism is alive and well. Markets will continue to function as they are made to do. The success of investment strategies, no matter how diversified, will have to succeed on their own accord. The price people pay for securities matters. Security analysis and its price discovery is more effective in matching price to value. When investors avoid active stock selection they can lose the free lunch that the S&P 500 Index can provide. On the discussion of price today and real returns of the future, investors may be Sharpe-ly disappointed.

Fear stock market failure,

Cole Smead, CFA

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Cole Smead, CFA, CEO and Portfolio Manager, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2023 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.