Dear Fellow Investors:

Globalization has created an interconnection between major world economies and commodity prices. China, as the world’s most populous country, rearranged the commodity landscape by growing their economy at double-digit compounded rates from 2000-2010. By doubling their use of oil, copper and other major commodities, China created a golden era for commodity investors and everyone involved in oil exploration and production.

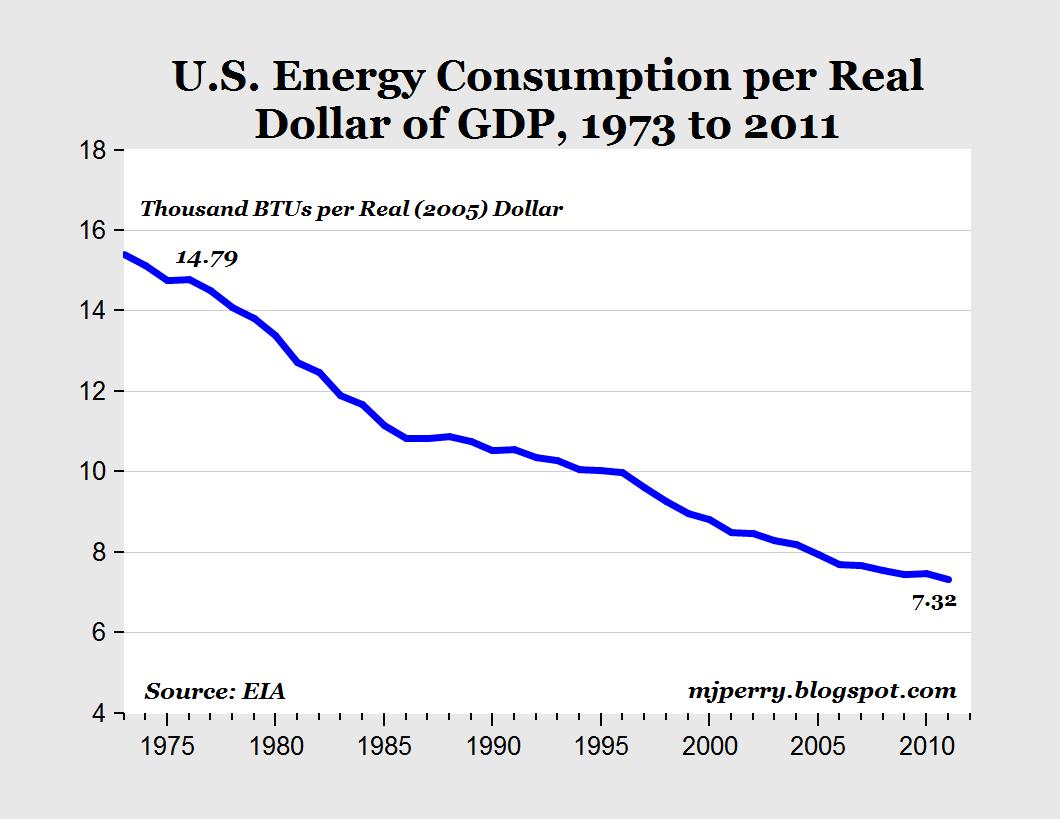

Thanks to dramatically higher prices for oil and major technological improvements in how we explore and produce oil, the supply and demand dynamics for oil sit in a very precarious position. We believe Brent crude prices above $100 per barrel are predicated on relatively uninterrupted economic growth for China and a vision of supply difficulty which current statistics argue against. On the demand side, the world’s largest user of oil, the U.S., has reduce its energy use to the point that it only takes $.07 of energy to create $1.00 of GDP. This is down from $.14 thirty years ago!

Even though we use dramatically less energy per dollar of GDP, gasoline is still a very important component in the composition of the consumer spending of the average U.S. household. Above and beyond the absolute expense are the key psychological factors. Everyone over the age of 35 in the U.S. lived in a period when gasoline was a much smaller part of the monthly budget. Higher oil and gasoline prices are a tax on U.S. consumers and it is no coincidence that our economy has struggled under the weight of a move up in gasoline prices from $1 per gallon in 1999 to over $4 per gallon recently. I can still see myself sitting in a gas line on odd/even days to buy the rationed 10 gallons in the oil embargo of 1974.

At Smead Capital Management, we believe that China’s uninterrupted economic growth, its emergence as a huge economy and the emergence of those countries which provided them with commodity inputs are the biggest difference between 1999 and today. To us, a diligent investor keeps an eye on what is going on in China’s economy for signs of a deeper slowdown. One piece of evidence came in late August from CNBC’s website in a blogpost called “China real estate: A bubble bursting.” Writer, Dhara Ranasinghe, makes the case that the slowdown in China real estate could create trouble for the Chinese banking system and the economy:

“The risks and exposure to property don’t look the same as in the U.S. sub-prime [mortgage crisis], but new bubbles never look exactly like the last bubble (otherwise they’d be easy to recognize),” said Patrick Chovanec, chief strategist at Silvercrest Asset Management.

“The exposure of China’s banks (and now shadow banks) to real estate may look different than it did in the U.S., but it’s very real. The main exposure is the reliance on property as collateral to support virtually all forms of lending throughout the economy, a situation that is very similar to Japan in the 1980s,” he added, referring to a collapse in Japan’s property market after a boom.

Jim Chanos and others have made the case that residential real estate and infrastructure spending make up over 55% of China’s GDP. Many experts have looked back into the history of other emerging economic powerhouses and recognized that high growth rates are unsustainable if infrastructure is at the heart of the numbers. It takes progressively more debt to create economic growth in China and represents diminishing returns, the enemy of staying power. Most investors and commodity market participants have watched this case being made for four years and have allowed it to be a “boy who cries wolf” argument. Since it has yet to come to pass, most investors think the risk of a China economic contraction is just something fringe investors or hedge fund managers concern themselves with. What would oil prices look like with the overconfidence in China no longer in existence?

At Smead Capital, we believe that business cycles are a fact of life for every major economy and that the longer China postpones the cleansing benefits of an economic contraction, the deeper contraction they are going to have. We also believe psychology plays a huge part in what happens, especially in pricing a commodity like oil. Therefore, we see the current supply and demand circumstances for oil preparing to ruin much of the 15 years of bull market activity which moved oil prices from $11 per barrel to Brent crude around $103 as we enter September of 2014. Here is a list of negatives for oil prices:

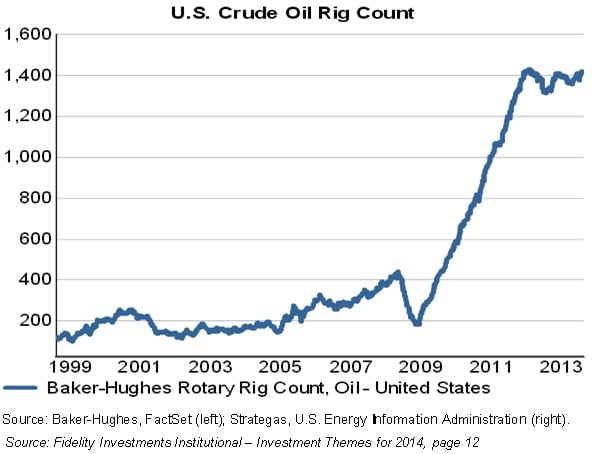

1. The U.S. has become the largest producer of oil and is possibly a net exporter

2. Every Tom, Dick and Harry around the world is drilling for oil and in many cases succeeding

3. Alternatives to gasoline are being pursued and adopted (think Tesla).

4. The U.S government mandates new cars boost mileage 50% over ten years.

5. Oil-producing nations like Brazil, Russia, Iran, Iraq and Venezuela need money.

6. Boom-bust states like North Dakota are booming.

7. Normally super-scary international turmoil hasn’t helped oil prices recently.

8. China’s economy is slowing even before the real estate bubble bursts.

9. Countries which supply oil and commodities to China are decelerating like Australia, Canada and Indonesia.

10. The U.S. Dollar appears to be making a move up and history shows that in the first nine months of interest rate hikes by the Federal Reserve, the dollar rallies 7% versus a basket of major currencies. A higher dollar automatically lowers the dollar price of oil.

The sad thing is we could go on. The good news is we don’t need to. The nature of commodity pricing is the positive and negative feedback loops which get going. In our opinion, a slowdown in China is inevitable (everyone suffers business cycles) and means a slowdown for commodity-producing nations. This could lead to lower oil prices and a break in the psychology which has supported the bull market in oil. If a negative feedback loop gets triggered by China’s recession, we would not be shocked to wake up in ten years with a move to $50 per barrel for oil sometime during that period. If we are correct, the U.S. economy, with its favorable demographics and the benefits of its successful deep-recession cleansing, would take the stimulating effects of lower gasoline prices and the psychological benefit to the consumer very well. The last time this happened was in the 1990’s.

Warm Regards,

William Smead

The information contained in this missive represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at smeadcap.com