Dear fellow investors,

At a minimum, the latter part of 2020 and the first half of 2021 will go down as one of the strangest psychological times for common stock investors. The euphoric mood has been overly apparent. While this is true for all ages and types of investors, younger investors (Millennials and Gen Z) have really stolen the show. We have a few interns in our office this summer. As we chat with them about the risk taking of younger people, we draw some conclusions. They love taking insane risks (crypto and options), but this is just like every age group was in the past when euphoric feelings were present. Love is in the air.

These young investors had adopted certain mantras. Maybe none more famous than the term “HODL.” HODL is short for hold on for dear life. What is striking to us is that, while the term is well-founded, they know that to create a large net worth you must hold a position for a very long time. This increases your net worth, while keeping the government away from taxing your unrealized capital gains. In effect, you just hold on as long as you can.

As an example, we commonly think back to what it was like to be one of Buffett’s partnership investors, who turned into Berkshire Hathaway owners in 1969, when he dissolved his partnerships and became solely the Chairman of Berkshire Hathaway. Buffett and Munger held the stock through thick and thin. Some may call this long-term common stock ownership. I think it’s better understood through the word Hodlvolk. It’s the people who are the long-term common stock owners. It’s the Hodlvolk. It’s a strange term when you hear it, but isn’t that what these long-term owners are? They are strange.

Using Berkshire Hathaway, we can see that investors had to watch over 50% of the value disappear between 1971-1975. Then, they watched the shares of the business go down 19% in 1981-1982. This was followed by a fall of 37% in the 1987 stock market crash. Then, in a déjà vu-like fashion, another 37% in 1989-1990. In the depths of the tech bubble, they had to watch the stock price decline 49% from 1998-2000. The 2007-2009 debacle caused a 51% decline in the value of Berkshire Hathaway shares. Lastly, the scare over the pandemic caused its value to decline over 30% in the spring of 2020.

Who would want to go through all these declines? Only the Hodlvolk survives. We do know the names of the Hodlvolk that went through all/much of this. We know Charlie and Warren were there. We know the Seqouia fund, David Gottesman, Phil Carret and handful of Buffett’s personal contacts in Omaha were part of the Hodlvolk. Did they know that they were going to compound capital at high rates? No. Did they know that declines were going to be extreme? No. All of these are unknowable in advance.

We could be sitting in a very similar juncture with our homebuilding stocks as we became involved with the sector with NVR (NVR) in 2013, Lennar (LEN) in 2016 and D.R. Horton (DHI) since the spring of 2020. The companies have rewarded us since we became owners from these points. Housing has made a demonstrable move in the minds of investors since the lockdowns of 2020. We have gone to a higher level of homebuilding than we had seen in the prior decade, which was a housing depression. Investors and professionals in the home building space are wondering if this is a short-term sugar high from the depths of last spring. They wonder if we can possibly continue to grow the housing segment or if this is a replay of the 2003 – 2006 bubble. Our problem with this short-sighted thinking is just that. It’s short-sighted. It’s representative of the type of owners swinging stock prices around in the short term. We are part of the Hodlvolk when it comes to these businesses. We think the future is bright and the demographics are amazing. Our three homebuilders have the largest share of US homebuilding they’ve ever had. Only the Hodlvolk survives.

We bring this up to remind all investors, but particularly investors that have entrusted their capital to us because it is a required practice. This is true regardless of whether it is Berkshire Hathaway or other wonderful companies that you might seek out as an investor.

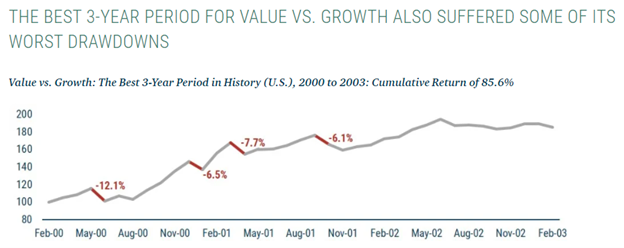

We proudly sit in the value camp. Value has seen a robust move over the last 12 months. Remember, as is true for our individual companies, it is also true for our portfolio. These things don’t go up in a straight line. GMO provided the great snapshot below as they looked at a dominate value era (2000-2003). During this time period value stomped growth by 86%. Who made this money? Only the Hodlvolk survives.

The market moved aggressively against the Hodlvolk investors from time to time. None of these drawdowns were enjoyable and they all made investors think twice about the value discipline they were practicing.

We are in one of those short-term periods where value has underperformed. Quality, growth and bonds have been rewarded in what we view as a counter-trend rally. These are the exact opposite of what we have seen over the last 12 months.

The talking heads of the futuristic growth world expound on what they think the market is telling investors. Warren Buffett says, “The stock market is there to serve you and not to instruct you.” In fact, he says, “The stock market is a device for transferring money from the impatient to the patient.” We would agree with him and add that only the Hodlvolk survives.

Warm regards,

Cole Smead, CFA

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Cole Smead, CFA, President and Portfolio Manager, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2021 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.