Dear Fellow Investors,

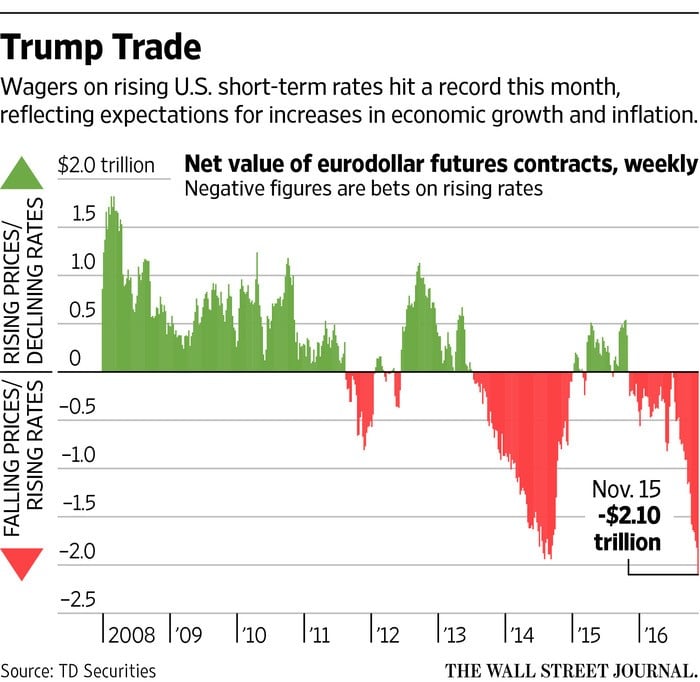

We at Smead Capital Management are in the camp of long-duration investors who believe we’ve entered an extended period of intermittent interest rate increases, a reversal from the 35-year era of intermittent declining rates we have experienced since 1981. The chart below shows that speculators have placed very heavy bets on rising interest rates in November.1 The placement of these heavy bets indicates that we could be close to the first temporary peak in the 10-year Treasury bond moving from the historically low rates around 1.5%. It looks to us like the first inning of a nine-inning game; the last game of this kind lasted 30 years.

We have also argued that the demographics of the U.S. dictate a stronger economy. We believe the economy will be led by a baby boom among 30 to 45-year old women and unusual spreads between housing affordability and rising rents. We think it is possible to create a tsunami of buyers nationwide and spur a housing boom. What will happen when the demand for houses and the nesting urge run into higher interest rates?

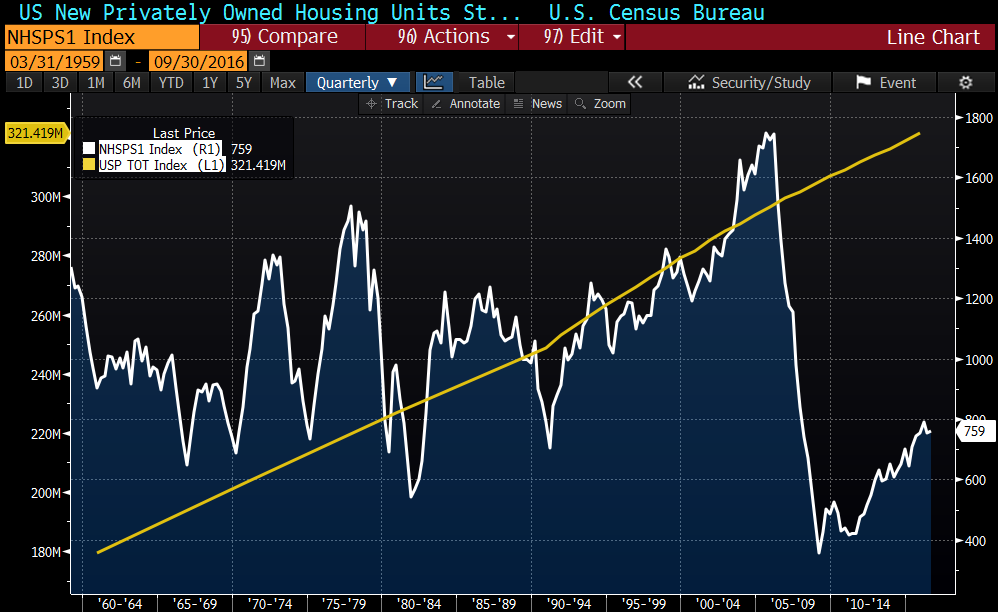

First, you have to look at history. The last housing boom was nutty in the early 2000s, because it was based on owning more than one home or owning a home the buyer couldn’t afford. The last boom propelled by actual household formation was in the mid-1970s. Baby boomers were getting married, having kids and defending themselves against rising inflation by purchasing a house. Of the homes lived in today in the U.S., our research shows that one out of ten were built between 1975 and 1980. As you look at these charts, remember that there are around 145 million more people living in the U.S. today than in 1960.2

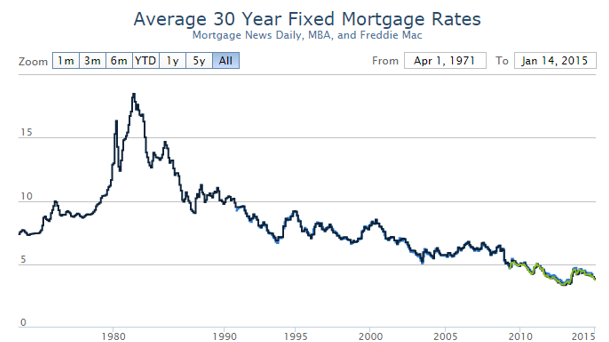

Furthermore, the last housing boom driven by household formation occurred at progressively higher mortgage interest rates. See the chart below:3

Therefore, if you want to buy a house to satisfy maternal and paternal instincts, it appears from a historical standpoint that interest rates and low levels of affordability don’t matter!

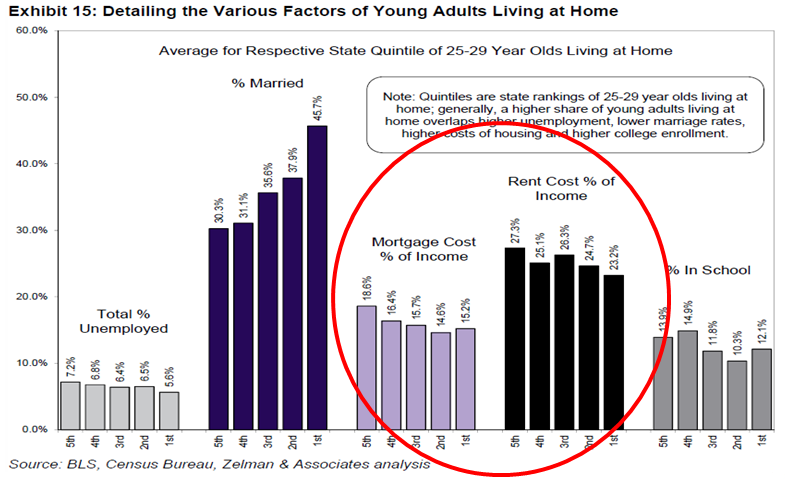

Second, you look at rent as a percentage of household income and compare it to the payments needed to own. As the following chart shows, the spread is looking pretty legendary.4

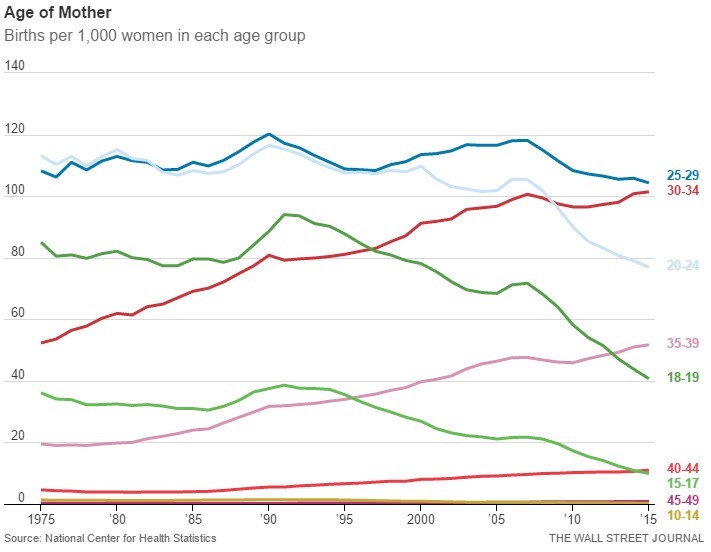

We like to say that the Millennial generation is living in Mr. Potter’s slums and that George Bailey won’t be alive until we are building way more than one million houses per year. According to the latest read in 2016, 759,000 homes were built in the last twelve months. There are 86 million Americans between 22 and 41 years of age. Home purchases among 25-to-35 year olds are half of prior generations, but very similar among those who are married and have children. The boom in births among 30-45 year old women means that we are headed to George being alive and homebuilding becoming “A Wonderful Life.”5

Apartment rents here in downtown Seattle give us a first-hand view of the nuttiness. There are 50% more cranes at work in Seattle than any other city in the U.S. They are used to build apartments to house new employees for tech companies like Amazon (AMZN), Facebook (FB), Google (GOOG) and Microsoft (MSFT). Unfortunately, this was a great idea ten years ago as the demographic wave was massed between 20 and 30-years of age. The chart below shows that the growth the next 15 years is in the number of 35-44 year old Americans, which means an explosion in the overall birthrate could occur.6

Lastly, our work begs the question whether American employees will begin to arbitrage housing affordability geographically or if companies will do so on their behalf. If a coastal city company were to move to the significantly less expensive 80% of the country, they would, in effect, give employees a massive benefit without spending money. This will matter a great deal when a crucial mass of millennials are married and have two kids. We might see many empty apartments in Seattle, San Francisco, Boston, Miami and New York if free market economics does its usual long-term stick.

In conclusion, the evidence suggests that the demand for housing, led by new families among 30-40 year old Americans, could overwhelm progressively higher interest rates. The long duration investor will be required to ignore the headwinds of higher rates as they own the businesses that could benefit from this wave of demand. As owners of some of these businesses, we feel that we are set up well to benefit from the high-quality companies that both meet our eight criteria and can be held throughout the coming home-building boom.

Warm Regards,

William Smead

1Source: The Wall Street Journal

2Source: Bloomberg

3Source: DoctorHousingBubble.com

4Source: BLS, Census Bureau, Zelman & Associates

5Source: The Wall Street Journal

6Source: BofA Merrill Lynch “Tracking the U.S. Consumer,” September 16, 2016

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2016 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.