“Don’t Believe the Hype.”

– Public Enemy

Dear fellow investors,

We have written a good deal about the parallels of today’s market with the tech and telecom bubble of the late 1990’s. While no two time periods are ever the same, today’s rhymes are eerily similar in some respects, with the latest development in initial public offerings (IPOs) as the latest example. Like past market peaks that ultimately corrected due to excessive valuation levels, markets are now working to suck in fresh capital as they sell the sizzle before anyone has tasted the steak (vegetable based or not). Today’s reverence for disruption and innovation have created such myopia that we might be beyond meat altogether.

A look back at 1999’s IPOs shows that 510 companies debuted and raised $65.9 billion in the United States stock market. This was the most in IPO history. It was also a 40% increase over 1998’s 363 deals, raising $37.5 billion, in other words, 75% more capital. To be clear, while 1999 brought some high-quality companies to market such as UPS, Conoco and Goldman Sachs, it also brought many more companies that never became good businesses and a substantial number that no longer exist.

The sizzle of 1999 sounded like hamburgers cooking on a hot grill. The top 10 IPO’s sorted by first-day performance was eye-popping: VA Linux Systems gained 698% in its first day, TheGlobe.com gained 606%, Foundry Networks 525%, FreeMarkets 483%, Cobalt Networks 482%, MarketWatch.com 474%, Akamai Tech 458%, CacheFlow 427%, Datatec (formerly Glasgal) 400%, and Sycamore Networks 386%. It’s rare that anyone from that era thought it would ever end. The prevailing mantra spoke of a new paradigm and the power of the new economy. Most all common stocks outside the new paradigm were heavily discounted. David Menlow of The IPO Financial Network, a company that has tracked the IPO market for years, predicted more frenzy for the year 2000 and afterwards, as an example.

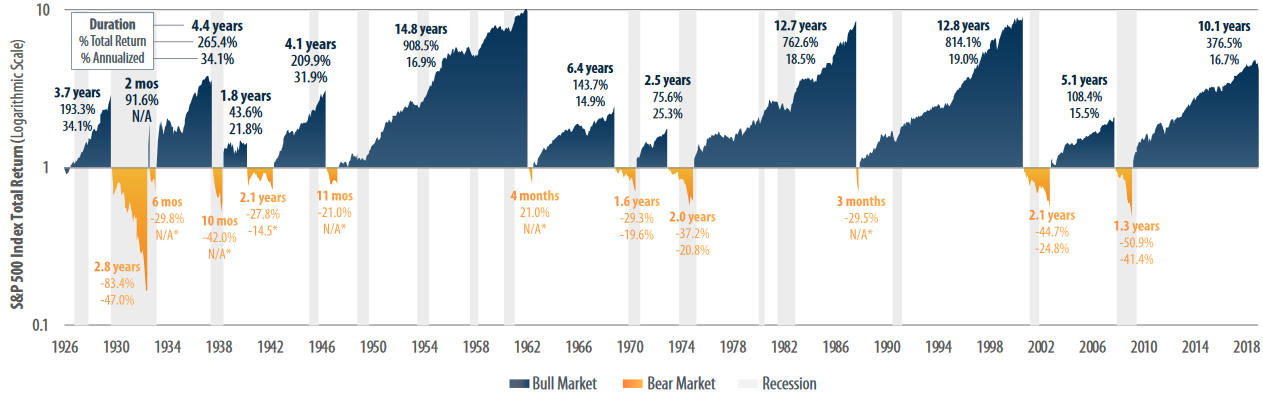

He and others may never have heard the Chinese proverb cautioning to be careful what you wish for. The market in early 2000 was dominated by Motley Fools. The frenzy that was foreseen indeed came about, but it wasn’t the kind anyone was looking for. The market leadership changes of 2000-2003 were of historic proportions, and Nasdaq stocks sat at ground zero. The IPO rhyme has played out consistently for other valuation-oriented bull market peaks too.

Source: FirstTrust Advisors

The value of all U.S. IPO’s issued in 1960 hit $178 million before dropping to less than $10 million by 1963. In the 1980’s, issuances grew from $640 million in 1984 to over $12 billion by 1987. This total shrunk by more than 40% two years later. Similarly, we issued $121 billion in IPO’s in 2007 with 409 deals, and only $26 billion on 161 deals by 2008. Looking at some of these stats, you might get the impression that the IPO window is as fickle as fashion trends. Welcome to the voting machine of the stock market.

One major difference in today’s rhyme is how long a company stays private before their public debut. Amazon’s IPO in May of 1997 came at a total market capitalization of $414 million for the entire company (it was $945 billion as of May 1, 2019). Even back then, that was a small-cap stock. Booking Holdings (formerly, Priceline) came in late 1998 with a capitalization of nearly $2.3 billion vs. today’s $81 billion. The initial equity holders made money on these, but nothing compared to the public! Fast forward, and we have deals like Lyft or Uber with initial market capitalization levels of $20 and $80 billion, respectively. Both have gone through the meat grinder and have left little on the bone for public consumption and benefit.

These facts and this history are not likely to stop Wall Street from sucking up massive amounts of capital as the IPO window is open wide. It does raise the question as to where the money will come from, because history has proven it comes out of the existing pool of common stock ownership. Think of it like this, the total supply of interesting tech and growth investments is rising dramatically and is providing dilutive choices to tech and growth stock investors in the public market.

As the party rocks on, many abandon the question of whether there is business merit worthy of long-term investment in these names. Could it be that the Motley Fools are back? Consider Uber, which touts 10+ billion trips taken over the last 12 months. This is eye popping considering it’s first trip was only seven years ago, yet it managed to consume $1.5 billion in cash from operations in 2018. Pinterest has been operating for nine years, yet has lost money each year, burnt cash, and offers the same in terms of the next few years of expectations.

Beyond Meat, a plant-based meat maker, may be interesting, but the market cap on its first day of trading was 9.3x bigger than Amazon’s when it came public. This is for a company which has only lost money and has mounds of competitors with very deep pockets. If that weren’t enough of a problem, a single supplier accounts for 79% of the input to its products and there are no fixed contracts for any co-manufacturers. As investors, it’s enough to want a little animal fat in your common stock portfolio.

We have no idea which of these thrilling new ideas will be winners or losers. What we can tell you is that we collectively have already been there and done that (but didn’t buy the tee-shirt!). As fun as all this IPO activity may sound, the voice of wisdom is speaking to us that it really isn’t different this time, this IPO window will close, and when it does it never ends well.

We sit with a set of very profitable companies which generate extremely high free cash flow. Ours offer strong economic value propositions with wide moats, most of which have stood the test of time and weathered many storms. We will patiently wait through fashionable investment trends, yielding to the long-duration merit of our investment criteria, and remind ourselves to not believe the hype.

Warm regards,

Tony Scherrer, CFA

Data source: MarketWatch

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Tony Scherrer, CFA, Director of Research, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2019 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.