The world we wake up to today seems to have all the information we can dream of, but less discernment than is needed. The Iran conflict was misread with oil prices at $100 and investors are doing the same thing at $70 oil now. We write this letter from the Calgary Stampede, one of the genuinely great events hosted globally. While we’ve been here, we have talked with all of the issuers we own in the oil business. The problem we are stampeding towards is real and time is the only cure.

There is talk going on right now that demand destruction is what is causing low oil prices at $70 a barrel. We advise our shareholders to not buy into this idea. The key issue is the crack spread, shown in the chart below. The crack spread measures profitability per barrel a refiner makes to create and produce products like gasoline, diesel and jet fuel. If demand destruction were going on, the refiners would see it first, and you would begin to see inventory builds in their products. However, these crack spreads argue that demand is incredibly strong.

Looking back over the last few years, we can take another big idea away. The first time we went over $100 oil in 2008 and ended up peaking at $147 a barrel on WTI, the world had trouble with oil that expensive. Demand destruction did show up and contributed to the ensuing financial crisis later that year.

In the 2010s, oil prices were often over $100 per barrel and yet we didn’t see large economic problems. We saw this again in 2022, interest rates rose significantly and we didn’t see a recession. We now see over $100 oil in the first half of 2026 and no recession is hovering over the economy. Investors have forgotten the fuel efficiency that has been reached in cars, planes, and other oil uses. These efficiencies lower the cost of doing anything with these end products and make the consumer less sensitive to movements compared to the past. We will refer to this as oil beta.

Oil beta has declined for the last 20 years, much like it has declined since the 1970s. Talking heads and people on Wall Street still treat $100 oil like it’s a golden calf and if we touch it, God will have Moses come down from the mountains and punish us. Oil is very important to the global economy, but the $100 price and its effect on oil beta sensitivities are not what they’re cracked up to be. If you just take an inflation-adjusted view of this oil beta idea, we would need to get to $220 a barrel to be analogous to the $147 oil of 2008.

On the companies we own in the oil and gas space in the fund, we couldn’t be more pleased with the opportunity ahead of them. As a reminder, we like the oil business. We like high reserve life businesses that show an ability to allocate capital well. We particularly like SAGD (steam assisted gravity drainage) oil assets, which Cenovus (CVE), Strathcona Resources (SCR), International Petroleum (IPCO) and Imperial Oil (IMO) have. Tamarack Valley (TVE) is a different asset, but are extracting heavy oil from water flood injections. We believe the opportunity is narrower in the oil patch of Canada today as the best assets sit in few hands. A good way to judge the evaluation of these businesses is by comparing the enterprise value to the flowing barrels they produce. It gives you a good sense of where everyone is priced.

These companies are producing strong returns on capital at $70 a barrel. We’d estimate this to be in the high teens, while they invest in growing marginal production on existing assets. If this is not good enough, the companies we own also prefer buybacks. This all comes to us while these businesses are trading very typically at two times the capital they need to run their business, or less.

The current oil problem of the last five years has been affording these companies much higher returns than they have historically produced because of the scarcity of new oil production. This scarcity continues to produce a lumpy, but higher return on capital than investors have ever seen.

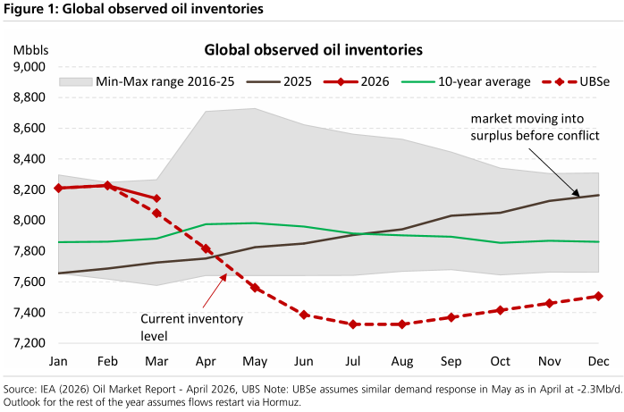

As we watch inventory draw globally in 2026, the real question is, will we have to see a large squeeze in the price of oil to get inventory to rise? While it’s possible that we could see a near-term price squeeze, the simpler math is that there will be 1 million more barrels of demand per day for the next three years to build up the inventory we lost to this point in 2026. Demand continues to grow at a very normal pace, which would be roughly 1 million more barrels per year needed. This means that in three years, there will be 4 million more barrels of demand from inventory or punishment and demand growth.

This sounds good, but there’s a catch. The United States has met the demand growth as the swing producer of the last 20 years. Supply is flatlining there and the question everyone is asking is what the decline will be going forward. Leave that flat for conversation’s sake. Canada would like to meet the 4 million barrel demand, but its production capacity can only meet a part of it in the near-term future. OPEC+ could do 1 million more barrels over the next three years also. Where do we get the other 2 million barrels? Price is the only thing that regulates supply. If we need more supply, we need higher prices. At $70 a barrel of oil, we are stampeding to the next problem: high oil prices over the longer term.

Play the Long Game,

_______________________________________________

The information contained herein represents the opinion of Smead Capital Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Arizona. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Registered investment adviser does not imply a certain level of skill or training.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

This Newsletter and others are available at smeadcap.com