Even before the war is over, the winning side needs to consider how to “win the peace” which will follow. The world has been fighting a war against the COVID-19 pandemic and as nearly universal vaccination approaches, investors need to think about how to win the peace. What does history tell us?

World War I

In the aftermath of World War I, the Allies punished Germany for its role as the main antagonist. Huge reparations were levied, and those financial claims put a big damper on the German population and its economy. This gave rise to Adolf Hitler and the Nazi Party in the 1920s and 1930s. In turn, the Allies ended up fighting another War in the 1940s, because they lost the peace.

World War II

The Allies learned their lesson from WWI. When Japan and Germany surrendered, the U.S. led an effort to shower grace on the German and Japanese people. To understand this, see a movie called Unbroken. When the Japanese waved the white flag, the U.S. dropped supplies into their enemy’s hands immediately. Also, the U.S. and its European allies developed the Marshall Plan. This helped the German and Japanese economy to thrive, and they became leading 20th Century economic powerhouses. We won the peace!

COVID-19 Pandemic

Since the War against COVID-19 isn’t won yet, investors are hesitant to think about “winning the peace.” The fight against the virus is affecting certain East Coast and Midwestern states much more than it is in states which have more heavily vaccinated and/or have seen a larger part of their population test positive for COVID-19.

Source: Fundstrat, CDC, World in Data and COVID-19 Tracking Project. Data as of 2/1/2021.

Therefore, it seems like a strategy for winning the peace makes more sense at the end of the first quarter of 2021, instead of trying to make any more money from fighting the war on the pandemic.

Who Won in the Pandemic?

FAANGs

Source: S&P, Yardeni Research Inc. Data for the time period 1/1/2013 – 2/2//2021.

Work from Home

Insane Speculation-SPACtacular

Source: Bloomberg. Data for the time period 1/1/1990 – 3/31/2021.

The biggest gains of 2020 came in companies which benefitted from the quarantines. This came through amazing moves in “disruptive” companies and a rush to capitalize on impatience by issuers of new Special Purpose Acquisition Vehicles (SPACs).

Animal Spirits

Source: Flow of Funds and JPMorgan. Data for the time period 1/1/1952 – 12/31/2020.

To say that the public and institutional investors have embraced common stocks would be a massive understatement.

Fleas and Lice

Source: Bloomberg. Data for the time period 3/31/2019 – 3/31/2021.

Charlie Munger was asked recently to compare Bitcoin to Telsa (TSLA). He said it “was like comparing a flea to a louse!”

Winning the Peace

Source: Fundstrat. Data as of 12/31/2017.

Too much money and too many people are chasing too few goods. This is the classic definition of inflation.

Source: Fundstrat. Data as of 12/31/2017.

We believe fortunes could be made satisfying these economic needs.

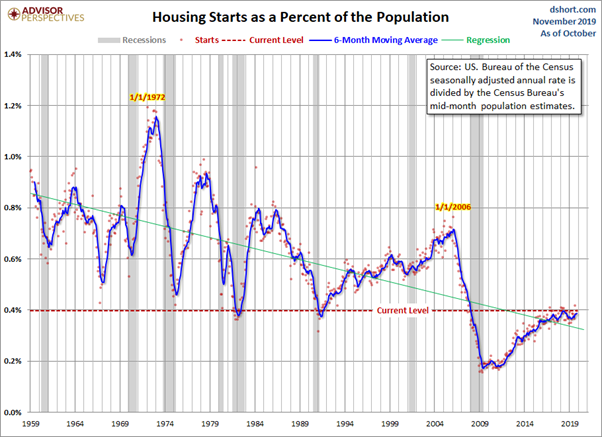

Main Street Economic Activity

Source: US Bureau of the Census. Data for the time period 1/1/1959 – 110/31/2019.

U.S. households have never been in better shape to borrow money.

Source: Bloomberg. Data for the time period 1/1/1979 – 6/30/2020.

Our eight criteria for stock selection and our vision of the next five to ten years of economic activity make us bullish on the homebuilders like Lennar (LEN), DR Horton (DHI) and NVR (NVR). We like Class A Mall REITs like Simon Property Group (SPG) and Macerich (MAC). The banks look compelling due to enhanced borrowing from millennial customers at American Express (AXP), JPMorgan (JPM), and Bank of America (BAC). American Express is heavily tied to business and pleasure travel and could have huge leverage going forward.

Oil stocks offer opportunity as the body politic restricts supply and attempts to make alternate energy sources more competitive. Drug/biotech blue chips are historically cheap in relation to the passive indexes. In January, Amgen reported that their most popular medicine, Prolia, had seen a 20% decline in new prescriptions from Q4 2019 to Q4 2020. It is not rocket science since Prolia is the most effective osteoporosis drug in the world and there are more baby boomers in that age group. This is the group that is most likely to get hit by osteoporosis than at any time in history. Therefore, they appear to be a bit of a reopening trade, because folks over 50 have been visiting the doctor less often and are being prescribed fewer new medicines. Vaccination should be solving this problem for these high-yielding blue-chip stocks.

Our portfolio has survived the war and is built to win in “the peace.” Thank you for trusting us as we attempt to avoid stock market failure in these relatively uncharted waters following a pandemic war.

The recent growth in the stock market has helped to produce short-term returns for some asset classes that are not typical and may not continue in the future. Margin of safety is the difference between the intrinsic value of a stock and its market price. The price-earnings ratio (P/E Ratio or P/E Multiple) measures a company’s current share price relative to its per-share earnings. Alpha is a measure of performance on a risk-adjusted basis. Beta is a measure of the volatility of a security or a portfolio in comparison to the market. FAANG is an acronym for the market’s five most popular and best-performing tech stocks, namely Facebook, Apple, Amazon, Netflix and Alphabet’s Google. Growth investing is focused on the growth of an investor’s capital. Leverage is using borrowed money to increase the potential return of an investment. Momentum is the rate of acceleration of a security’s price or volume. The earnings yield refers to the earnings per share for the most recent 12-month period divided by the current market price per share. Profit margin is calculated by dividing net profits by net sales. Quality is assessed based on soft (e.g. management credibility) and hard criteria (e.g. balance sheet stability). Value is an investment tactic where stocks are selected which appear to trade for less than their intrinsic values. The dividend yield is the ratio of a company’s annual dividend compared to its share price.

The information contained herein represents the opinion of Smead Capital Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Arizona. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Registered investment adviser does not imply a certain level of skill or training.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

This Newsletter and others are available at smeadcap.com