As a young stockbroker in the 1980’s, I was hungry for disciplines which could help me make money for clients. One of the most sensible things I came across was a theory by an investor that we refer to as the 70-20-10 rule. Human nature dictates an urge to make money in stocks quickly and for me that was proving to be difficult and problematic. Hence, the hunger to learn from theories like this rule.

Part one of the rule said that in the next 12 months, the return you got on a stock was 70% determined by what the U.S. stock market did, 20% was determined by how the industry group did and 10% was based on how undervalued and successful the individual company was. Part two of the rule said that over ten years, 70% of how you did would be determined by the valuation and success of your company, 20% by how the industry did and 10% would be determined by how the stock market did.

With the formation of Smead Capital Management in July of 2007, we made an obvious commitment to part two of the rule. We thought it would be helpful to understand why.

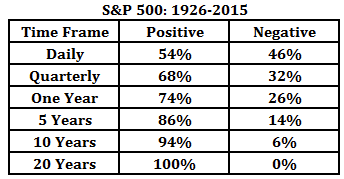

- The stock market is unpredictable. The chart below shows how much your U.S. stock market results and the reliability of the results are enhanced by long-duration time frames:

Data for the time period 1/1/1926 to 12/31/2015 - Short run stock moves are random. Many of our best ideas over the long haul took three years or more to develop. We knew all about a compound called Denosumab, which ultimately produced medicines called Prolia and Xgeva, in 2011. Nobody cared about their maker, Amgen (AMGN), at $52 per share until they started paying dividends and doing massive stock buybacks. It still looks cheap to us at around $166 per share on October 3rd of 2016.

- Psychological reversals take one to three years. We buy quality securities at steeply discounted prices, but the reversal of severely negative psychology can take a decade. Just ask the major U.S. banks, which continue to be a whipping post for politicians and angry former investors.

- Operating in one-year time frames forces high portfolio turnover. The average large-cap U.S. equity fund turns its portfolio over 62% per year and causes trading costs of around .81% annually.1 In an era of lower returns, this could cost investors a big part of their results.

- Short holding periods invite the IRS into your life. Net short-term gains are taxed at ordinary income tax rates and the maximum tax on long-term gains is 23.8% with the surcharge. Long holding periods for winning common stock holdings may avoid years of taxation.

What is the obvious downside of using part two of the 70-20-10 rule? First, it is a guarantee that you will have stretches of significant market underperformance. A study of five of the greatest long-term investors of all time (John Templeton, Phil Carret, Warren Buffett, Peter Lynch and John Neff) showed that they underperformed the stock market 35% of the time and it usually occurred in two-year bunches.

Additionally, part two of the 70-20-10 rule requires you to make no effort to avoid the bear markets in stocks which have happened about once every five years, historically. We believe that those who operate in ten-year time frames and have high-quality common stocks with consistently high free-cash flow will either be abused less in major declines or spring back to life much faster in the aftermath.

The last and maybe most important ingredient for practicing the 70-20-10 rule in long durations are your investors. We think Seth Klarman, lead manager at Baupost Group, says it well:

“We have great clients. Having great clients is the real key to investment success. It is probably more important than any other factor in enabling a manager to take a long-term time frame when the world is putting so much pressure on short-term results.” — Klarman at the 2010 CFA Institute annual conference.

CNBC writes, “The investor repeatedly says his biggest advantage is having long-term-oriented clients. He remarked that it is impossible to invest for a three- to five-year holding period, if you’re worried clients may redeem in six months.”2

Many of you should be familiar with the history of our Capital Appreciation strategy. We started managing accounts in early 2008 at the beginning of one of the biggest equity declines in U.S. history. We purposefully hold less than 5% cash in our portfolio. Our assumption is that we give our investors a long-duration U.S. large-cap value stock portfolio. We assume our job is to seek alpha as compared to the benchmarks over five to ten years. We make every effort to communicate with our investors in a way which helps them stay in place for five to ten years or more.

We are in one of those time periods where practicing under the 70-20-10 rule (part two) makes investors uncomfortable. We position our holdings for maximum long-term success and ignore money making opportunities outside our discipline, especially ones where maniacal pricing and crowd favor are involved. The great stock picker Robert Rodriguez said it this way:

“I believe superior long-term performance is a function of a manager’s willingness to accept periods of short-term underperformance. This requires the fortitude and willingness to allow one’s business to shrink while deploying an unpopular strategy.”3

Part one of the 70-20-10 rule would have dictated an investor bail out of the stock market in 2008-2009. It also would have sent investors packing in the summers of 2010, 2011, 2012 and 2015. Remember, when 70% of your results are determined by the direction of the stock market over six to twelve months, it makes you a trend follower and it puts the onus on things you don’t control and can’t predict. Outstanding patience is required to succeed when you operate under the 70-20-10 rule part two!

We are very realistic about the investment marketplace while many are becoming committed to owning the stock market via the S&P 500 Index. We are not surprised that investors operate out of the first part of the 70-20-10 rule and/or have thrown their confidence for the long haul toward the index. Two arguments we’ve made recently lead us to believe that the 70-20-10 rule argues for part two.

First, the most expensive stocks in the S&P 500 Index are the most overvalued in relation to the average stock and the cheapest stocks since the tech bubble broke.

Source: Smead Capital Management as of 8/1/2016. Forward P/E ratio is a current stock’s price over its “predicted” earnings per share.

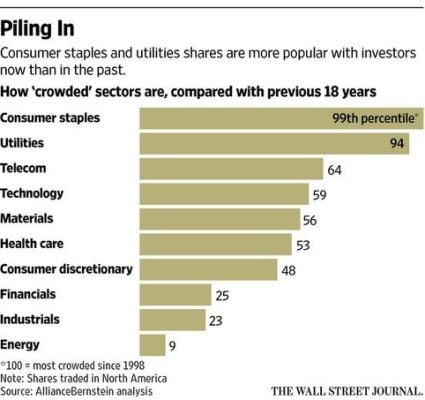

Second, we have argued that low interest rates have spurred over-investment in high dividend stocks being purchased as bond surrogates and have helped prevent the “animal spirits” from juicing the U.S. economy. Thanks to research from Alliance Bernstein, we have the following chart which shows how crowded together active investors have become compared to the last 18 years.

Source: The Wall Street Journal as of 7/31/2016

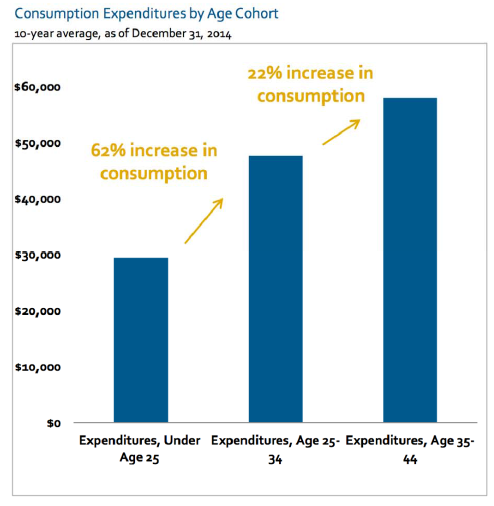

Where do we see the opportunities over the next five to ten years under the 70-20-10 rule part two? Our eyes turn to 86 million Americans between the age of 22 and 41, knowing it is a guarantee they will age ten years by 2027. Therefore, we are on the cusp of a 15-year stretch in the growth of the 35-44 year old age group.

Source: BofA Merrill Lynch Global Research, Euromonitor as of 9/16/2016. Y axis represents U.S. Population age 35-44.

Marriage, increased birth rates, home buying and car buying could be followed by consistently higher levels of household spending as millennials move into their 40’s.

Source: Morgan Stanley

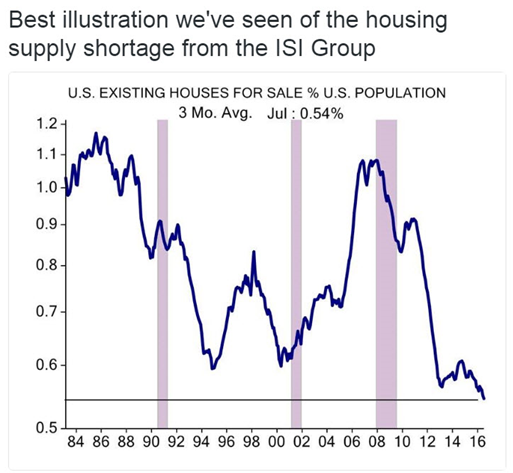

The U.S. economy has been in an anemic recovery ever since 2009 with little or no help from household formation, birth rates or home building. Today, there is a massive pent up demand which starts with homes for sale at a legendary low point versus the total population (see chart below). Demand for mortgages could explode and are the single biggest source of borrowing (60% of household liabilities) in the U.S. economy.4

Source: ISI Group as of 7/31/2016. Y axis represents percentage of U.S. Population. Blue line represents houses for sale per U.S. Population. Shaded areas represent recession periods. Black line represents 3-Mo. Average as of July 2016.

In a dramatically better economy, there could be completely different winners in the U.S. stock market. Investors have loved tech, staples, utilities and other ways to succeed in a lower for longer interest rate environment absent of meaningful economic growth and what John Maynard Keynes called “animal spirits.” We are on record that interest rates are headed higher and those rates will be set by the millennial population demanding credit, not the Federal Reserve Board actions closely watched by most investors.

We appear to be going from a nation of single Americans between 20-30 years of age, to married with children. Craft beer makers, restaurant and bar owners, fast and casual dining establishments and others could lose in the demographic shift. Eating at home, supplemental health insurers and professional journalism providing local news could be winners.

We always operate under the assumption that valuation matters dearly, we must own businesses for a long time and to do this means we must own high quality companies. The 70-20-10 Rule demands that we do bottoms-up stock picking in long durations to get to part two of the rule. We think equity investors will be well served because of the way things have played out over the last 18 months. We thank you for your confidence and willingness to operate in historically successful time frames.

1Financial Analyst Journal, Jan/Feb 2013, by Roger Edelen, Richard Evans and Gregory Kadlec

2Source: CNBC

3Source: FPA Funds

4Source: Federal Reserve Z-1 Report

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Washington. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results.There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications. For additional information about SCM, including fees and services, send for our disclosure statement as set forth on Form ADV from SCM using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

This Newsletter and others are available at smeadcap.com